Here in Portland, OR, we have our fair share of happy hours. I don’t go to them so much anymore, but the general idea is that restaurants or bars will offer discounted food and drinks to fill seats during slow business hours. The great thing about happy hours from a customer perspective is that you get more value for your money. It’s a sale on food and alcohol… what isn’t to like?

The same can be said for the stock market as well. Stocks can be expensive, and stocks can be cheap. You want to buy when stocks are cheap and sell (or just maybe buy less) when they get expensive. The goal of getting a good deal on stocks is called value investing, and trying to buy when stocks are cheap and sell when they are expensive is called market timing.

A word of caution

Timing the stock market is generally frowned upon by financial advisors and popular media, and for good reason. Timing the market is hard, stressful, risky, and requires discipline (and even with discipline it sometimes backfires). It probably isn’t something the beginner or casual investor should even worry about.

The most important thing that beginner or casual investors should focus on is saving regularly and saving a lot. It isn’t necessary to know how to time the market to be a successful investor. In fact, many people say it is next to impossible.

And as a reminder, I am by no means an investing expert myself. This is just my take on it all.

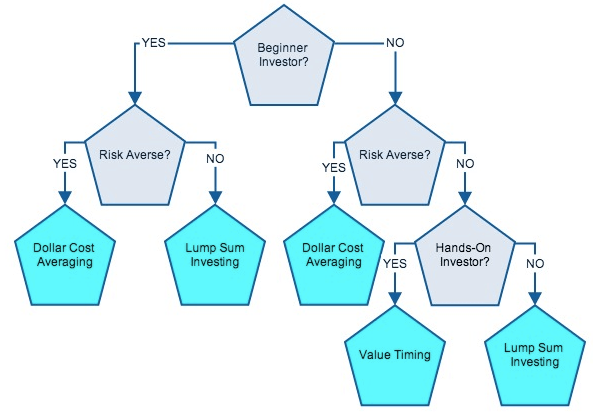

Investment strategy decision tree

Below is a decision tree that might help guide someone between three different investment strategies that I will summarize later: dollar-cost averaging, lump sum investing, and value timing.

A brief note: even though it might look like it in the decision tree above, these strategies aren’t mutually exclusive. You can combine them in a bunch of different ways, which I will discuss at the end.

Investment strategies

1. Dollar Cost Averaging

Keeping with the happy hour theme, think of the dollar cost averager as the Irish worker that stops by the pub for one pint of Guinness everyday on her way home from work. Even on a tough day, she never has more than one.

Anyone with automatic 401k paycheck deductions is a dollar cost averager whether they like it or not. The idea of dollar cost averaging is that you invest the same amount of money on a regular and somewhat frequent basis. With 401k paycheck deductions, this strategy is almost inevitable because you don’t really get to make the investment timing decision yourself (of course, Mad Fientist has a hack for this).

But let’s say that you get a $6,000 tax return. Do you invest it all at once now, do you invest it all at once later, or do you invest it in bits and pieces (dollar cost averaging)? The advantage of investing it in bits and pieces, say $500 every month for a year, is getting to spread your risk. For example, the market could crash in month 3, making stocks a much better deal than they were earlier. And as a dollar cost averager, this means you get 9 months of happy hour stock prices that you wouldn’t have had otherwise.

Compare this to the person who invested the whole $6,000 right away. Depending on how bad the market crashed, the investment might only be worth $4,500 now.

Bottom line: dollar cost averaging is highly recommended for the risk averse investor.

2. Lump Sum Investing

If the dollar cost averager is our daily drinker, the lump sum investor is our payday partier. Every Friday our gal takes her hard earned money to the pub for five pints of Guinness with friends. So using the $6,000 tax return example from above, the lump sum investor puts all the money into the stock market right away.

The advantage of investing the whole $6,000 right away is that you have the potential to capture compounding stock market gains for the rest of the year. But the knife cuts both ways because you have the potential to capture major stock market losses too, like in the example above. This is what makes lump sum investing riskier than dollar cost averaging.

So which strategy has a higher expected average return? Luckily Vanguard already ran the numbers for us. They looked at a moderately conservative asset allocation of 60% stocks and 40% bonds and found that after 10 years, on average, the lump sum investor had about 2% more money than the dollar cost averager. Lump sum investing outperformed dollar cost averaging in about 2/3 of all historical periods. But what about the risk, you might ask? What if you happened to invest during the other 1/3 of historical periods where lump sum investing underperformed?

Well, Vanguard has an answer for that too. Even after adjusting for risk using the Sharpe Ratio, lump sum investing is still the clear winner (versus dollar cost averaging). What this means is that the higher average returns from lump sum investing are not due to excess risk, they are actually due to a smarter investing strategy.

Bottom line: if you can tolerate more risk, lump sum investing is probably a better way to go than dollar cost averaging.

3. Value Timing

Starting of course with another drinking metaphor, the value timer only goes to the pub when she can get there early enough for happy hour Guinness specials. However, when she does go, she has a few extra pints to make up for any missed opportunities earlier in the week. The same thing can be done with the stock market, and if you do it right, with less of a hangover to boot.

The idea behind value timing the stock market is simple. Buy when stocks are cheap; don’t buy when they are expensive. It is like vacationing in the off season… you end up spending less on flights, food, and lodging, but your overall experience is still pretty much the same. But how do you know when stocks are cheap? More on that below.

Bottom line: value timing is best suited for someone willing to invest a little more time and energy into their investment decisions and also for someone willing to deal with more risk and ambiguity. This is not an ideal strategy for passive, casual, or new investors. Even a lot of experienced investors choose to stay away as well.

Market valuation and the PE ratio

Baron Rothschild famously said, “the time to buy (investments) is when there’s blood in the streets.” He was ahead of his time in the sense that he recognized how irrational investors can be. Rothschild knew that there were two relevant components of a stock, price and value.

Time to invest? I can picture Baron Rothschild listening to this as he prepares to pwn other investors. Image courtesy of Wikipedia.

Owning stock means you own part of a company’s assets and future earnings. This is the value piece. Price, on the other hand, is one step removed from value.

Price is the dollar amount people are willing to buy or sell their company ownership for, and Rothschild knew people could be pretty irrational about these kinds of financial decisions. One of the most common irrational investor behaviors is buying when the market is hot and selling when it is cold.

For example, during the 2008 stock market crash, a lot of people panicked and sold stock after market prices had already fallen significantly. As more and more people behaved similarly, stock prices sunk even further.

This is not an ideal investment strategy for the medium to long-term investor (aka the average individual investor). These people were taking a major loss selling their stock at happy hour prices, and the cooler heads in the room were more than happy to buy this unwanted stock at a discount because they recognized that the underlying value was still there.

So what is the best way to measure underlying stock price value? It is pretty easy to spot a market sell-off and act accordingly, but what about spotting an overheated market? The most common way to measure relative stock market value is to look at the price to earnings ratio (PE ratio).

The PE ratio is exactly what you think it is. Divide stock price by company earnings. A low PE ratio means that, relative to earnings, the stock price is pretty reasonable, maybe even on happy hour special. A high PE ratio means that the stock is more likely to be overpriced.

The PE ratio isn’t a perfect predictor of value because company earnings are historical, while stock prices are largely forward-looking (future earnings, remember). But it is still a good directional tool, especially the Shiller PE ratio.

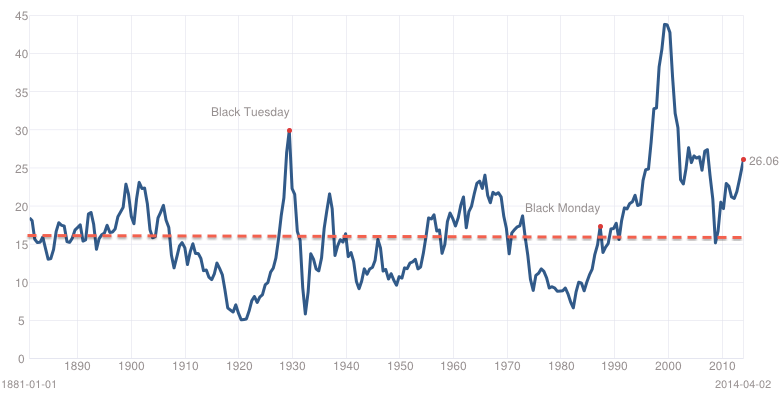

My favorite PE ratio for the overall stock market is the Shiller PE ratio, also known as the cyclically-adjusted PE ratio (CAPE ratio) or PE 10. The Shiller PE ratio calculates average, inflation-adjusted earnings over the past 10 years instead of just looking at most recent earnings. Using 10-year historical earnings removes a lot of seasonality from the data and theoretically improves accuracy.

Here is what the Shiller PE ratio has looked like for the S&P 500 (an approximation of the total U.S. stock market) since the late 1800’s:

As you can see, the Shiller PE ratio has averaged 16 for the past 100+ years, and as of 4/2/2014, the ratio stood at 26, indicating that stocks were definitely not on sale.

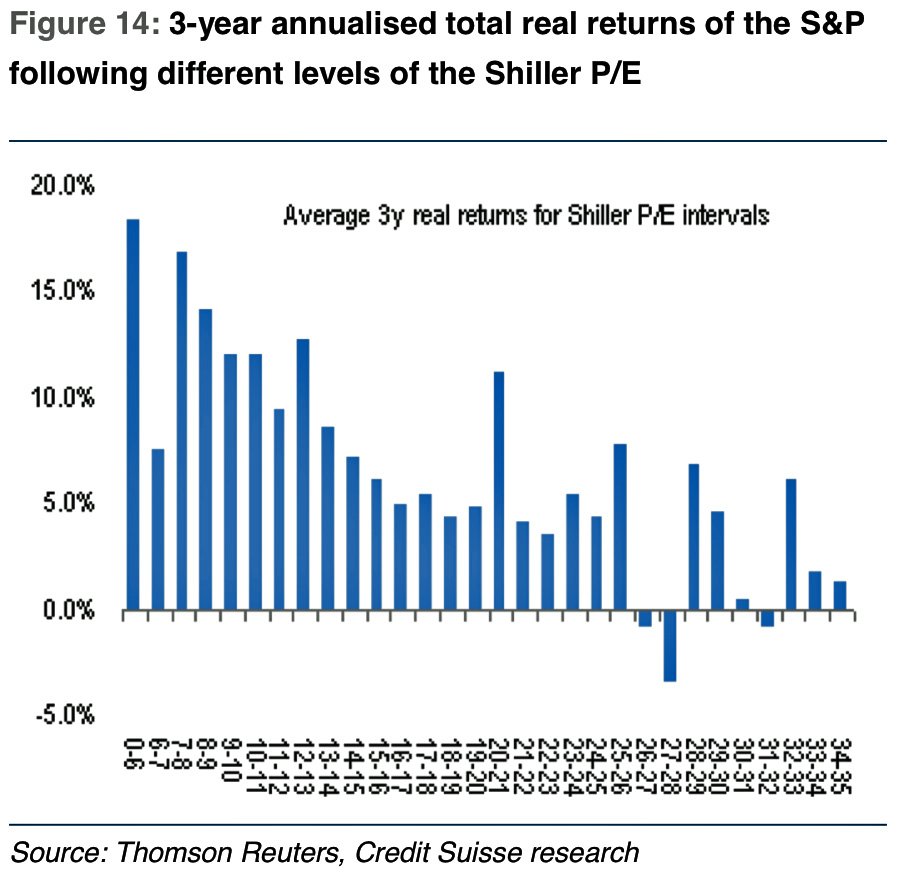

Does this mean that you should dump all your stocks for cash? Probably not. The Shiller PE ratio IS NOT about timing market crashes as it is about predicting future returns. Business Insider borrows a nice chart from Credit Suisse illustrating this relationship:

This chart measures returns over the relatively short timeframe of 3 years, but Shiller’s original study used a 10-year timeframe. Either way, the relationship looks pretty strong, and I imagine it would look even stronger if we could see the same thing over 10 years.

How to use value timing

The general rule of thumb is that the lower the Shiller PE ratio, the more you should invest. The higher the Shiller PE ratio, the less you should invest. At VERY high ratios, some would even suggest that you move some of your stocks into bonds or maybe even cash if you are really pessimistic. A really fancy, more complicated take on value timing is called value averaging.

Personally, as a young investor, I’m not a fan of taking money out of the stock market nor sitting on the sidelines, regardless of valuation. I am more concerned with how to put my money in. During VERY low Shiller ratio times, I will throw every spare cent at the stock market because stock market happy hours don’t seem to be that common anymore.

A former teacher of mine had an even simpler approach. He said that you will never know what will happen with the stock market tomorrow, but you do know what happened yesterday. And if the stock market dropped by 5%+, you are getting a much better deal than you would have the day before, so invest. And if it drops 10%, invest even more enthusiastically.

In addition, you can blend certain strategies. For example, it is 4/2/2014 and the Shiller PE ratio is pretty freakin’ high, almost the second highest ever. I just got my tax return and want to use it to contribute to my IRA / Roth IRA this year. After sleeping on it, I think my strategy is going to be to dollar cost average for the next 8 months, and if the market drops by more than 3-5% over a few days or a week, I will invest the remainder all at once.

My logic is that the market is expensive, and dollar cost averaging might spread my downside risk a little bit until I can find a short break in what has otherwise been a pretty bullish market. The biggest risk here is missing out on continued growth during my dollar cost average period. Here is an example of how it would ideally work (it is always easier in hindsight):

The circles represent times I would (in an ideal world) make a lump sum investment, the other times I would dollar cost average. This is my ad-hoc expensive stock market strategy.

UPDATE: This was a sub-par strategy, and I eventually changed course to lump-sum. I did capture a few “bargains” first, but the market just kept growing and I was missing out on that growth by sitting on the sidelines. My main mistake was forgetting that high-PE ratios don’t necessarily predict more frequent downward market price shocks. As mentioned above, a high PE is more useful as a predictor of future returns, which are, on average, almost always positive. Please see my new post about timing the stock market for more information.

You can also use market valuation to make non-investment decisions. One of the best unintentional moves I ever made was to withdraw a lot of my retirement stock to pay for graduate school. I sold the stock about a year before the 2008 market crash, when stocks were much more expensive. Based on my back of the napkin calculations, I saved over $10,000 with that move.

My wife and I are actually having a similar discussion right now. Travel is a big priority for us, and it would be nice to get one last big trip in before we start having kids. Given how expensive stocks are right now, our opportunity cost of spending a little extra money versus investing it is probably smaller. Is that a sign that we should go? (hint: flannel gal hopes you say yes 🙂 )

Other applications include helping decide if you want to pay off your mortgage (or student loan) earlier or invest more money in the stock market. Depending on your mortgage rate, it probably makes more sense to invest when stocks are cheap and to pay more of your mortgage when stocks are expensive.

And for someone lucky enough to be thinking about retirement, now could be a great time to rebalance your portfolio to a heavier bond position, if that is something you already plan on doing for retirement anyways. The logic is the same, stocks are expensive, and you will get a good price on them. Lock in your gains now.

Hopefully those are enough examples to get the wheels turning. As I said before, I’m no market expert, but this is what I have gathered from some 80/20 research and my short career as an amateur investor. I encourage you to investigate further and have listed some more sources below.

Further reading:

- Dollar-cost averaging just means taking risk later | Vanguard

- Dollar cost averaging | Bogleheads

- Value averaging | Bogleheads

- Choosing between dollar cost averaging and value averaging | Investopedia

- How investing dimes can beat dollars | Wall Street Journal

- Is dollar cost averaging overrated | Morningstar

- Challenging dollar cost averaging and other bad ideas | NY Times

- Robert Shiller: Jan 2014 – I’m still investing in the stock market | CNBC

- You’re not listening to Robert Shiller if his CAPE ratio has you scared of stocks | Business Insider

- Market Timing for Value Investors | The Arbor Investment Planner (has some other valuation measures besides Shiller PE)